Could transporters run out of diesel?

For South African transport and logistics operators, diesel is the lifeblood of the industry, dictating operational costs, fleet efficiency and profit margins. However, a perfect storm of global supply chain disruptions and looming local energy constraints is threatening the very availability of this critical fuel.

“Diesel has always been South Africa’s ‘last line of defence’ for energy security, but that assumption is now at risk,” warns Dominic Goncalves, advisory partner for Energy Strategy at Cresco Project Finance and founder and director of Naviara Energy.

For decades, the trucking industry was able to rely on a steady, albeit expensive, stream of fuel. However, as the global disruption in the Strait of Hormuz enters its sixth week, the transport sector is being exposed to a severe vulnerability. The reality is that South Africa is no longer the self-reliant fuel producer it once was.

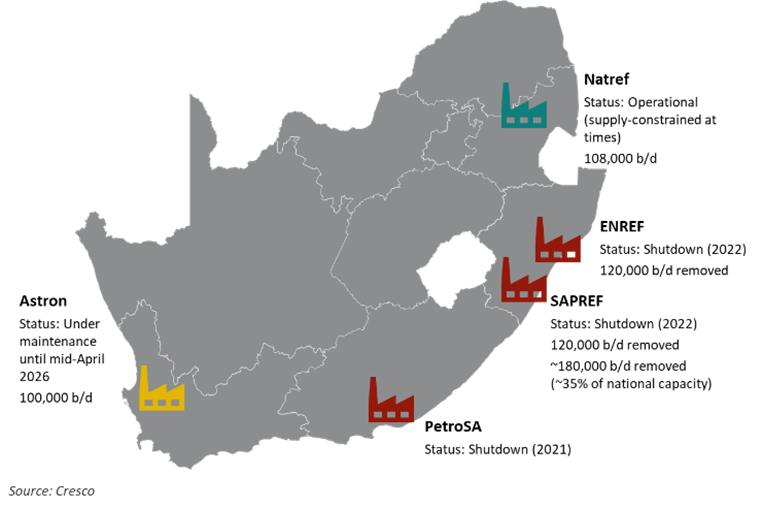

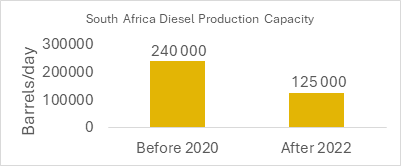

As Goncalves explains: “Since 2022, South Africa’s domestic diesel refining capacity has halved – the shutdowns of SAPREF and ENREF have turned South Africa from a relatively self-sufficient refiner of diesel products to a structurally import-dependent country (70 to 75%), exposed to global diesel markets and highly sensitive to shocks like the Hormuz disruption.”

The global bidding war for your fleet’s fuel

Transport operators are no longer just fighting local economic pressures; they are directly exposed to geopolitical fallout. “More than half of South Africa’s diesel is currently imported from Gulf suppliers directly exposed to Hormuz disruption, such as Oman (34%), UAE (12%) and Bahrain (11%), or indirectly exposed to Hormuz disruption via supply chains such as India (20%),” notes Goncalves.

With global supply chains fracturing, South African importers are being forced to fight for fuel on the international stage. Fleet owners will ultimately bear the brunt of this competition. Goncalves highlights the stark reality of this global squeeze: “SA is having to compete for non-Gulf barrels against stronger buyers such as Asia and Europe. India is acting as a swing supplier, reallocating barrels to the highest-paying market (Asia).”

While South Africa has not yet declared a national diesel shortage, transport operators are already navigating “pricing shocks, logistics disruption and localised shortages”.

Published by

focusmagsa