Air freight braces for further potential market shocks in 2026

Air freight braces for further potential market shocks in 2026

Despite one of the most uncertain years for global trade and economic policies in over 20 years, the 2026 Air Freight Outlook report from market analytics platform Xeneta notes that air freight ended 2025 in a stronger position than many expected. Nevertheless, 2026 has the potential for further market shocks.

The Xeneta report, authored by the company’s chief airfreight officer Niall van de Wouw and lead airfreight development and analyses Wenwen Zhang, notes that early warnings of air cargo demand collapse and supply-chain shocks gave way to steadier, if uneven, expansion. Air cargo demand finished 2025 with a modest 3 to 4% growth, but weaker market sentiment led air cargo rates to decline by an estimated 1 to 2%.

The World Trade Organization (WTO) predicts a dramatic deceleration in merchandise trade – from 2.4% in 2025 to 0.5% in 2026 – as the full effect of tariffs and inventory corrections hits global trades. The report says air freight – historically more volatile than the economy it serves – will likely feel this shift acutely, and identifies seven key themes shaping the year ahead.

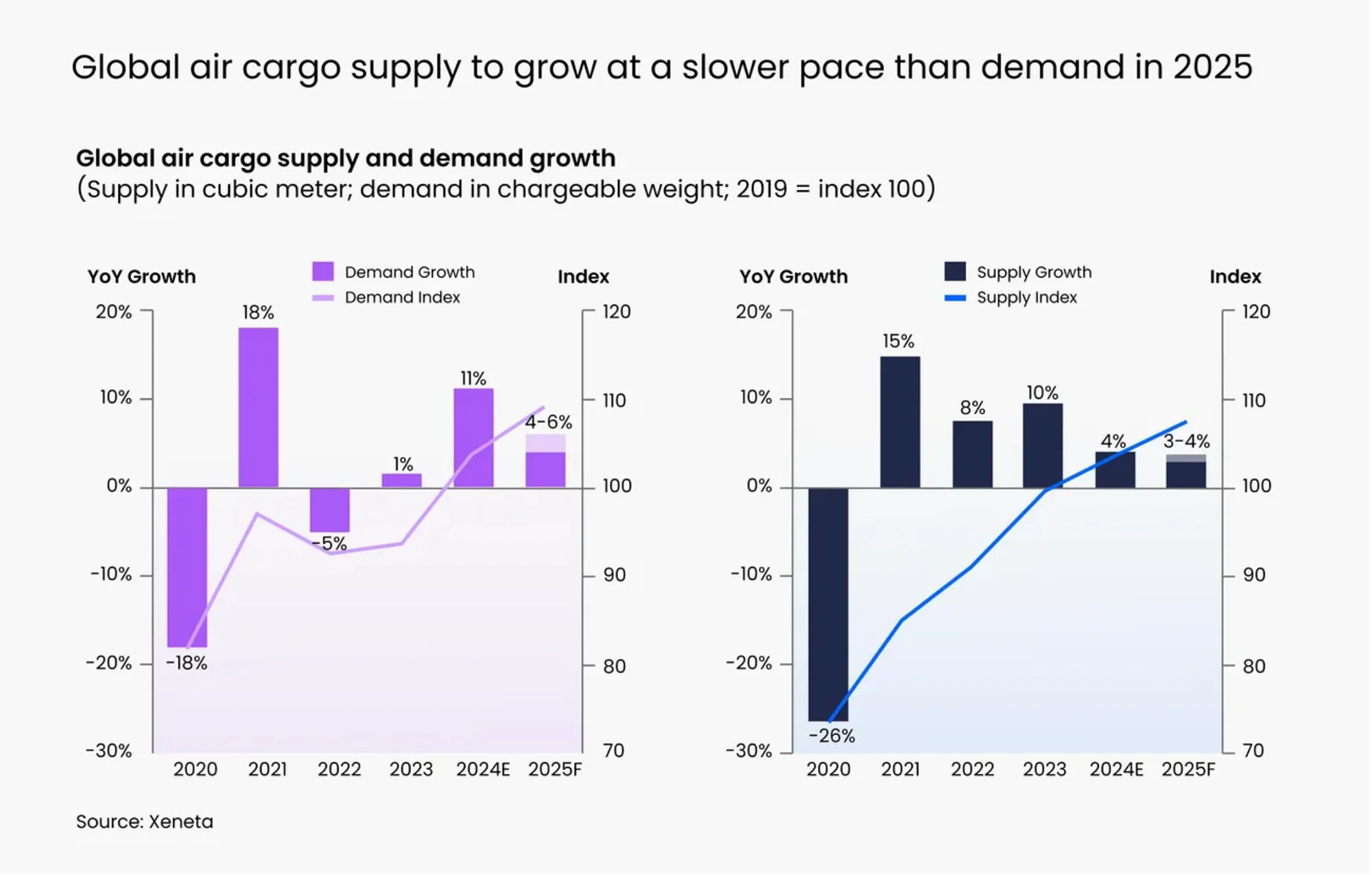

1. Slowing world economy to dampen air freight growth, but differences exist across corridors

Air cargo demand in 2026 is likely to fall back in line with the global economy, despite air freight volatility and disruptions in supply chains and trade policy. Much of the apparent air cargo demand strength in 2025 reflects mode-shift relating to frontloading, e-commerce and AI growth, while uncertainty over US tariffs triggered firms to bring imports forward, temporarily lifting goods flows and air cargo volumes to avoid higher tariffs. With inventories swelled, however, this is inherently unsustainable.

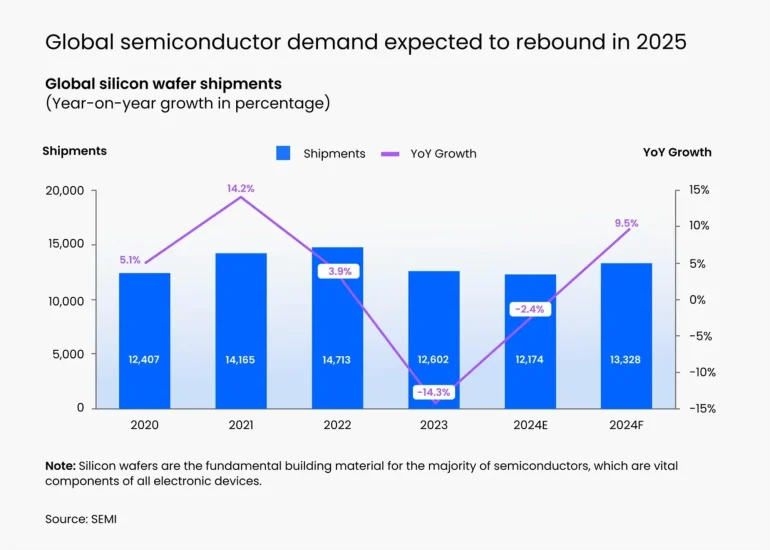

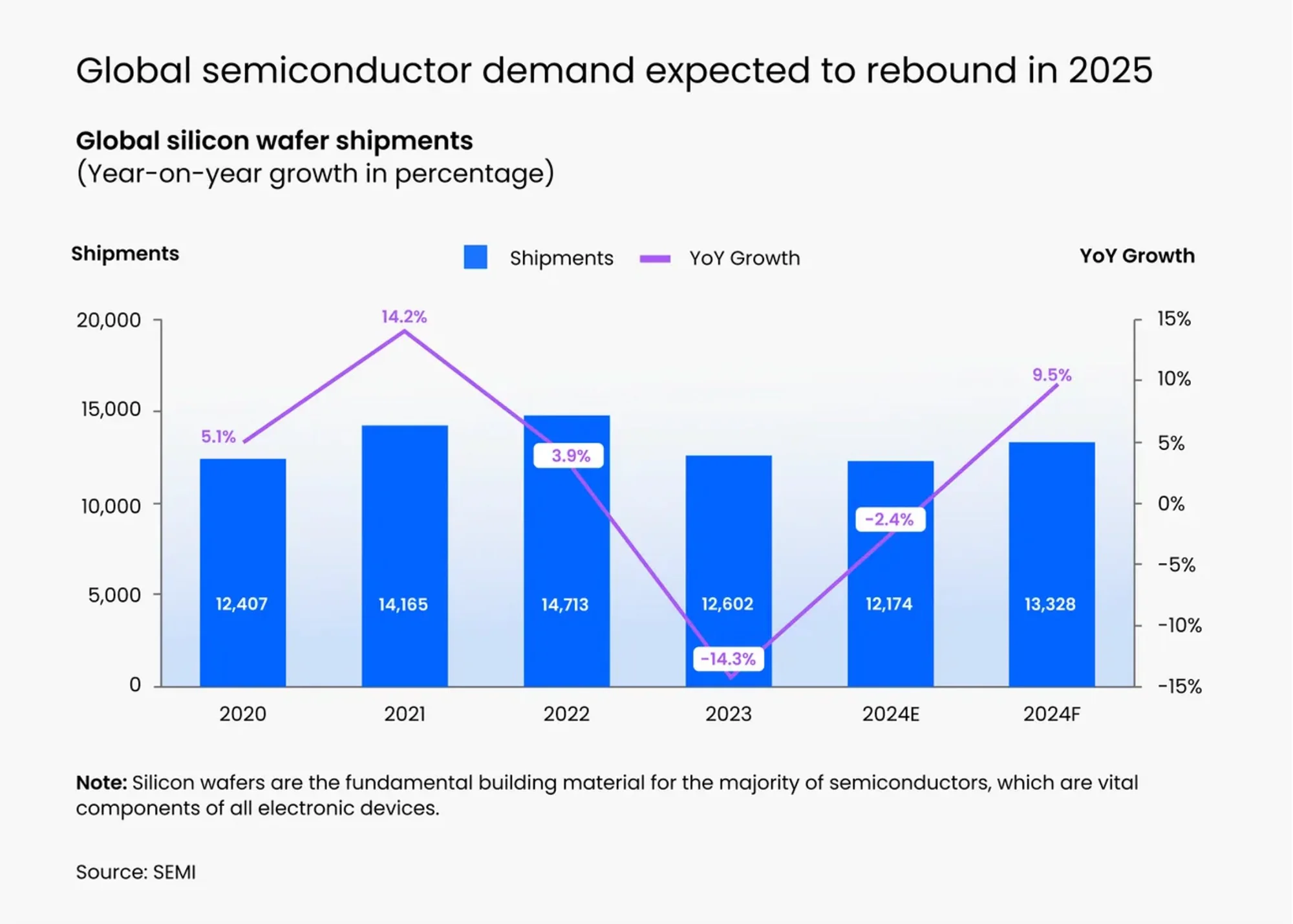

Modest growth in global GDP sets the tone for the general air freight market in 2026 (excluding the more buoyant e-commerce and AI-related semiconductor air freight shipment niches). Traditional air cargo segments have been stuck in the doldrums for several years. Even silicon-wafer shipments for non-AI applications are only just beginning a tentative recovery from a recent downcycle.

The Europe–North America corridor, less exposed to the recent e-commerce boom, illustrates this downward pattern for more traditional air freight sectors. EU to US air cargo volumes dropped to their weakest level in two years (-6% year-on-year) by October, as inventories built ahead of tariff hikes adversely impacted import volumes.

Global trade patterns are being rewritten in the wake of geopolitics; air freight lanes are reshaping accordingly. US–China trade continues to weaken, with air cargo demand on the Asia–North America lane contracting and the Asia–Europe corridor emerging as the stand-out performer. Southeast Asia is benefiting from direct investment from China and US–China trade tensions, absorbing relocated production with double-digit growth in air cargo volumes, while Taiwan is expanding outbound volumes tied to hi-tech and semiconductor industries.

These shifts are already altering air cargo rate movements. The East Asia–Europe corridor, with strong e-commerce and semiconductor exposure, is experiencing only modest downward pressure on rates, while those tied to easing ocean shipping disruptions (Europe–Middle East & South Asia) and trade policy changes (East Asia–North America) are seeing sharper freight rate declines.

2. More regulated e-commerce

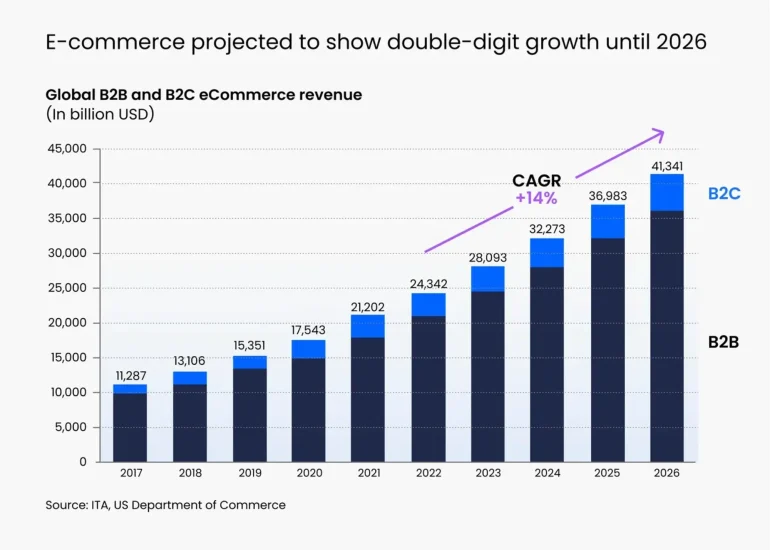

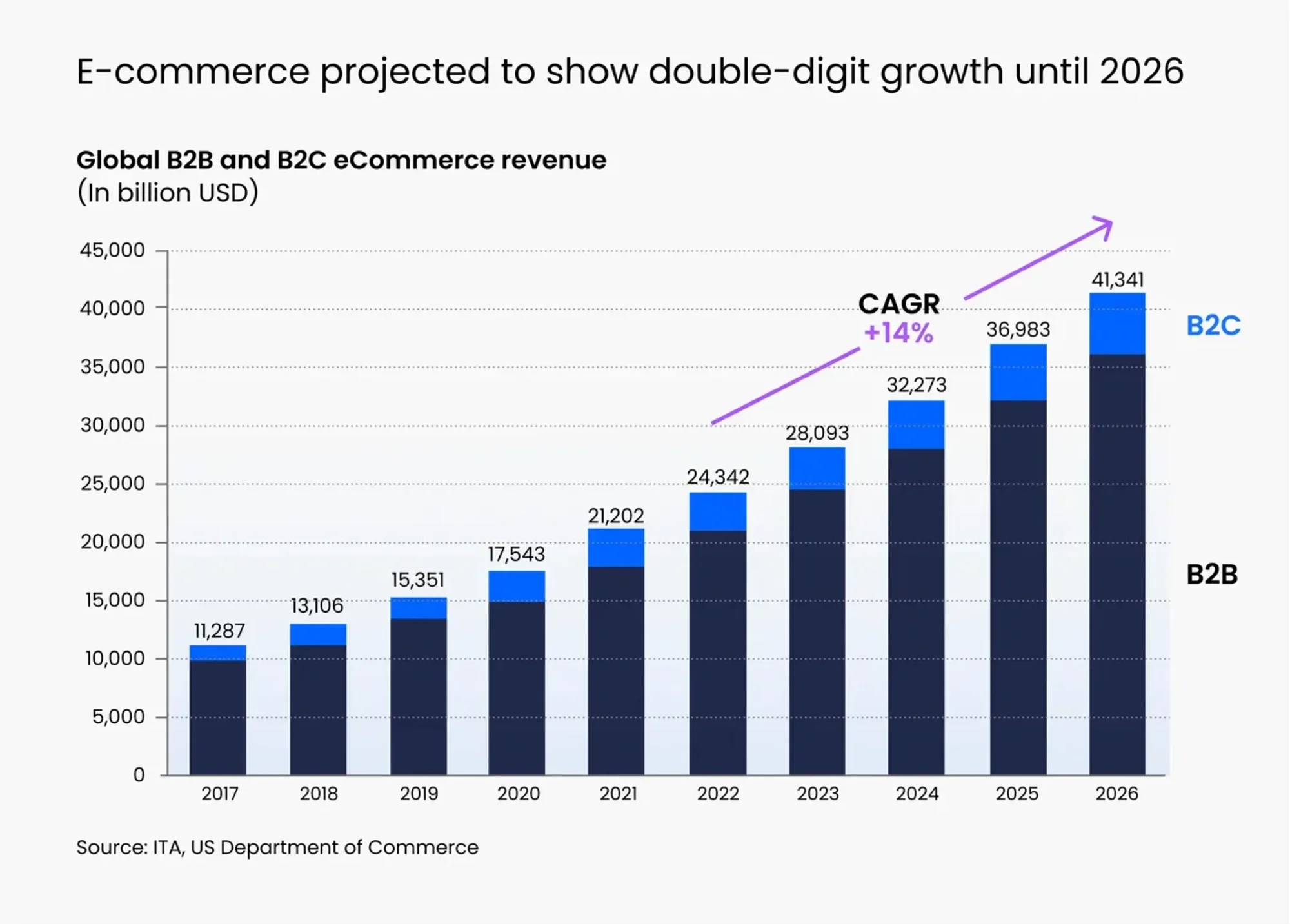

E-commerce remains the most dynamic force shaping global air cargo demand over the past few years, with its scale and rapid adaptability to trade policy shocks continuing to surprise observers.

Since the US scrapped de minimis exemptions for Chinese parcels in early May 2025 and for all countries from late August, low-value e-commerce shipments from China (roughly 3% of global air cargo volumes) have declined.

Shippers’ rational response to pressures is to sacrifice air freight’s speed in favour of slower, lower-cost ocean freight. They may also adopt a hybrid mode, reserving air freight for runaway bestsellers when demand spikes.

Despite disruptions, Chinese e-commerce volumes have been diverted from the US to other markets (particularly Europe) with impressive responsiveness. There are, however, some warning signs. After 27 straight months of near 40% year-on-year growth, China’s total cross-border e-commerce sales were flat in October, while robust expansion to Europe was offset by declines to the rest of Asia and the US.

Cross-border e-commerce will face a more regulated landscape in 2026, primarily in the US and EU, while nations including Japan and Thailand have also discussed or announced new rules commencing in 2026. E-commerce volumes are thus likely to grow more slowly, but still faster than the general air freight market, with platforms continuing to respond to policy changes and shifting trade flows.

3. Mode shift due to easing pressure in ocean container shipping

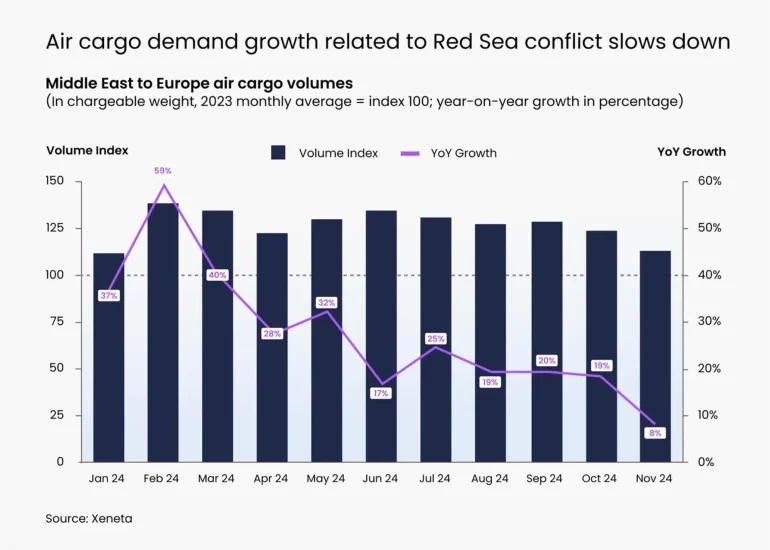

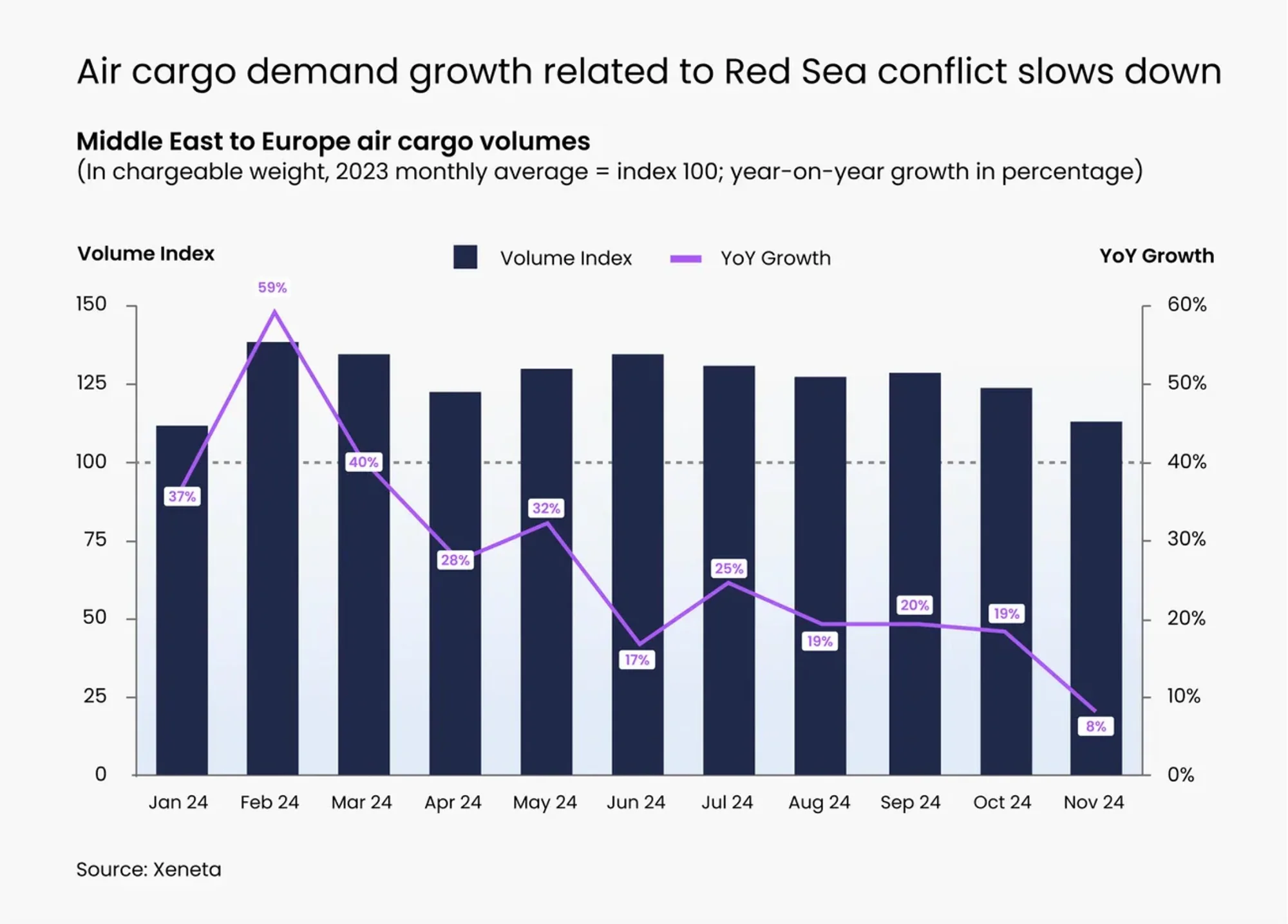

Air freight’s historic advantage lies in its ability to provide shippers with resilience during periods of global disorder – be it supply chain disruptions or geopolitical tensions. The Red Sea disruptions of 2023 to 2025, coupled with tariff-related frontloading into the US, gave air cargo a sharp uplift as container ships were forced around the Cape of Good Hope, ocean schedules deterioriated and rates increased. This made airfreight more price-competitive and resilient, adding to the motivation to shift mode.

That advantage is unwinding as ocean shipping schedule reliability slightly improves. A large-scale return to the Suez Canal route in 2026 could reduce the global fleet’s required transport and increase shipping capacity by around 15%, with air-to-ocean shift unavoidable. However, ocean shipping networks would need two to three months to readjust schedules, potentially causing severe port congestion and (for a short period) redirecting some volumes back into air freight.

Over the longer term, structural ocean container shipping overcapacity is the overriding factor. With a record orderbook for new vessels and subdued demand, ocean rates are likely to remain depressed. This weakens the rationale for using air freight, with increasing predictability and reliability combined with lower ocean container freight rates dragging basic machinery, auto parts, low-end electronics and apparel back into ocean transport, except in moments of geopolitical shock.

4. Growing influence of AI-related demand bubble

Artificial intelligence (AI) is fast becoming a major engine for air cargo demand growth. The WTO reports that 43% of global merchandise trade growth in the first half of 2025 came from AI-related goods (semiconductors, processors, finished computers, servers and telecoms kit), despite these accounting for only about 15% of total trade.

The surge has been broadly spread, with the US and Asia taking the lead. Much of this cargo is high-value, time-sensitive hardware – key air freight selling points – putting AI investment at the centre of demand in 2026. On key lanes such as Taiwan–US, air cargo volumes registered double-digit growth in 2025, a clear imprint of the AI boom.

The forecast for semiconductors tells the same story, with 2025’s rebound in silicon wafer shipments driven by AI, while as noted in the introduction, non-AI applications are only just emerging from a downcycle. It is estimated these shipments will grow 5.2% in 2026 and continue climbing through 2028.

AI-related demand is likely to continue outpacing the muted macro forecast, representing a direct boon for air cargo. J.P. Morgan estimates major American tech firms will lift annual capital spending from US$150 billion in 2023 to over US$500 billion in 2026, much of this on AI data centres and their connection networks. AI-related investment is already around 1% of US GDP. Investment in previous waves of general-purpose technologies (railways, electrification, telecoms) often peaked at 2 to 5% of GDP, suggesting room for the AI build-out.

Public policy is pushing in the same direction: big-ticket programmes. The US “Stargate” initiative, Europe’s InvestAI schemes and China’s directed credit give the boom for air freight even more credibility. However, there is, of course, the question of AI bubbles. Global watchdogs are cautious that the AI boom is starting to look less sure, with lofty private valuations and exuberant funding rounds. “The big question is how long will the AI investment boom continue? It does not seem to be running out of steam just yet… freight forwarders and airlines should keep a close eye on it, as the current market could change… with little notice period,” advises Zhang.

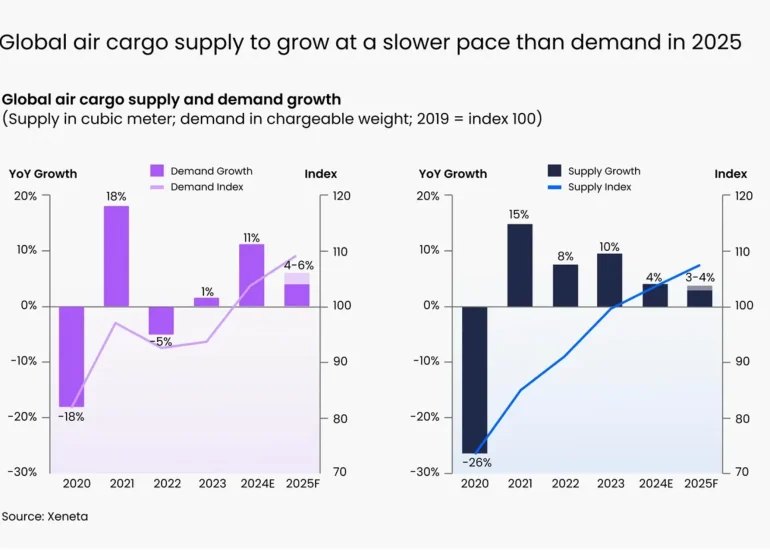

5. Air cargo capacity growth to exceed demand growth

The air cargo market is likely to face excess capacity in 2026 but at a relatively low level. Xeneta forecasts global air freight capacity to grow 3 to 4% in 2026, exceeding overall air cargo demand growth of 2 to 3%.

In 2025, Rotate reported that increased freighter aircraft capacity utilisation drove about half of the growth in freighter capacity (with limited room to continue in 2026), with the other half from new deliveries. In terms of passenger belly capacity, accounting for just over half of the international capacity, the scheduled capacity growth has been increasing at a slightly slower pace, which is expected to continue into the new year.

Long-term structural bottlenecks in capacity growth – such as production delays in widebody aircraft deliveries that are unlikely to be resolved until 2027-28 – will provide some relief for carriers by keeping the capacity-demand ratio tighter than it would have otherwise been. However, supply will still outpace demand growth, so yield pressure is unavoidable, especially on lanes with heavy belly exposure.

6. Industry dynamics – freight rates expected to fall

Global air cargo freight rates could fall 5 to 10% in 2026, depending on geopolitical and economic factors. For airlines, this uncertainty shifts the relationship with freight forwarders away from long-term contracts towards something more dynamic and transactional. With increasing capacity and a slower-growing pie, airlines will double down on dynamic pricing, yield management and granular lane-by-lane optimisation.

Forwarders, sensing a buyer’s market, will be even less willing to sign long-term, fixed-rate block space agreements. Spot and short-validity contracts will gain further ground as forwarders wait for rate declines rather than commit volumes. Airlines, in turn, will try to claw back commitment and continue efforts in dynamic pricing to optimise revenue and adjust freighter capacity more effectively to market changes.

Shippers may respond by sacrificing the speed of air freight in favour of cost-effective ocean container freight, or hybrid sea-air and consolidation models. Whenever a shipper does utilise air freight, they will also demand that every decrease in airline rates flows through almost immediately to their buy rates.

The forwarder–shipper relationship will become more data-driven and focus on cost controls. Shippers will increasingly use external rate benchmarks, load-factor analysis and capacity indicators to challenge quotes, rather than relying on relationship pricing.

Contract structures between shippers and forwarders are also evolving, such as index-linked agreements with formulae tied to airfreight price indices. 2026 is going to be a tough market for forwarders, so they must justify their margin and demonstrate value-added service differentiation to secure shipper volumes. This includes greater visibility and transparency, exception management and customs expertise.

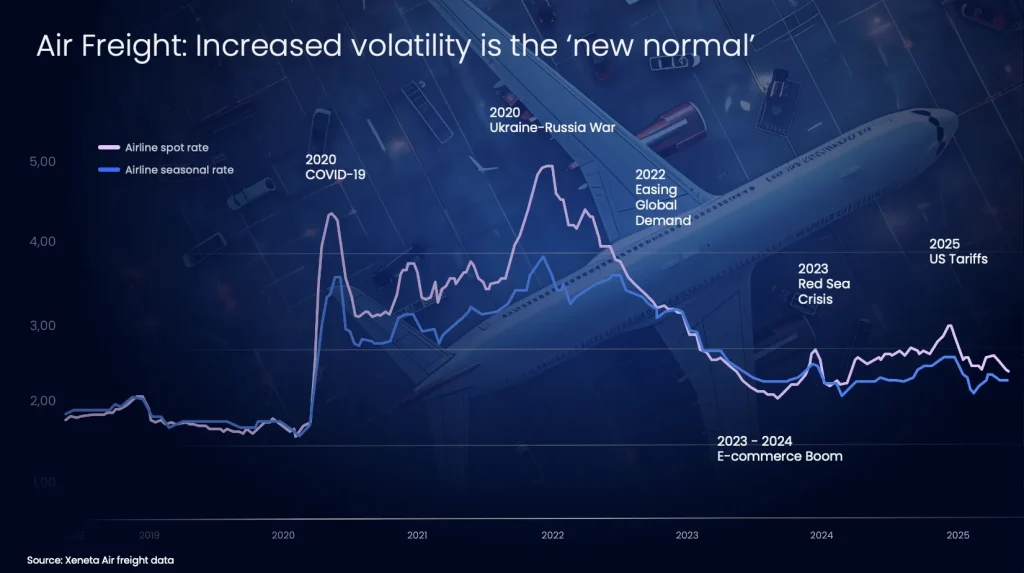

7. Wildcards – the new normal of global logistics

Whether it is geopolitical conflict in the Middle East, the Ukraine-Russia conflict or tension in the South China Sea, threats to global supply chain stability, airspace availability and insurance costs are constant. Climate events, cyberattacks on logistics networks and renewed tariff escalations add to the wide array of potential market shocks in 2026.

“The lights on the risk dashboard will be flashing red in 2026 and the outlook for airfreight could change dramatically if we get another Black Swan event. It would be a brave person to bet against this given the events of recent years,” warns Van de Wouw.

If so, the subdued forecast for air freight could be radically changed with little or no warning, so retaining flexibility and understanding of supply chains at a global, regional and corridor level across modes will be more important than ever in 2026.

Published by

Focus on Transport

focusmagsa

{kind=link}

{kind=link}

{kind=link}

{kind=link}