Unpacking the fuel levy

Here’s a look at how the fuel levy was initiated and how its utilisation evolved.

Between 1925 and 1935, government decided that the funding of national roads would no longer be subsidised by provincial and local authorities. Hence, it was decided that public road users would be taxed. This resulted in the establishment of a National Road Fund in 1935 to fund mainly national roads for national development and unity. At the time, a percentage of the import tax from every litre of fuel imported (three pennies per gallon) went to the fund.

Even after subsequent increases in the levies, it became apparent that the National Road Fund needed more revenue to be able to repay National Treasury bonds. It also needed money for the construction of urban highways (in Johannesburg, Cape Town, Durban, and Port Elizabeth).

In 1961, it was decided that the fund would acquire income from a tax on all imported and locally-produced petrol, diesel, oil, and paraffin. Over the next 12 years, it was planned that the fund would distribute 60% of the income for construction or reconstruction of national roads and bridges. A further 12% would be spent building new urban freeways in metropolitan areas, while 11.5% was reserved for assisting on special roads and 8% for maintenance.

However, with the decrease in fuel consumption resulting from savings regulations due to international sanctions, the fund experienced dwindling revenues. Hence, by the 1980s, tolls were introduced to fund new roads or road improvements on stretches where an alternative route existed. The introduction of tolls would come as an additional cost to road users but was “sold” to transport operators (to soften the blow) as a means to have dedicated funds for roads and infrastructure (amongst other competing state expenditure).

During the period 1983 to 1988, as promised, we were fortunate enough to see a dedicated, ring-fenced fuel levy, in addition to tolls. In 1988 however, then-Minister of Finance Barend du Plessis amended the legislation, changing the ring-fenced fuel levy to a general levy, where the income could be used for other government expenditure programmes.

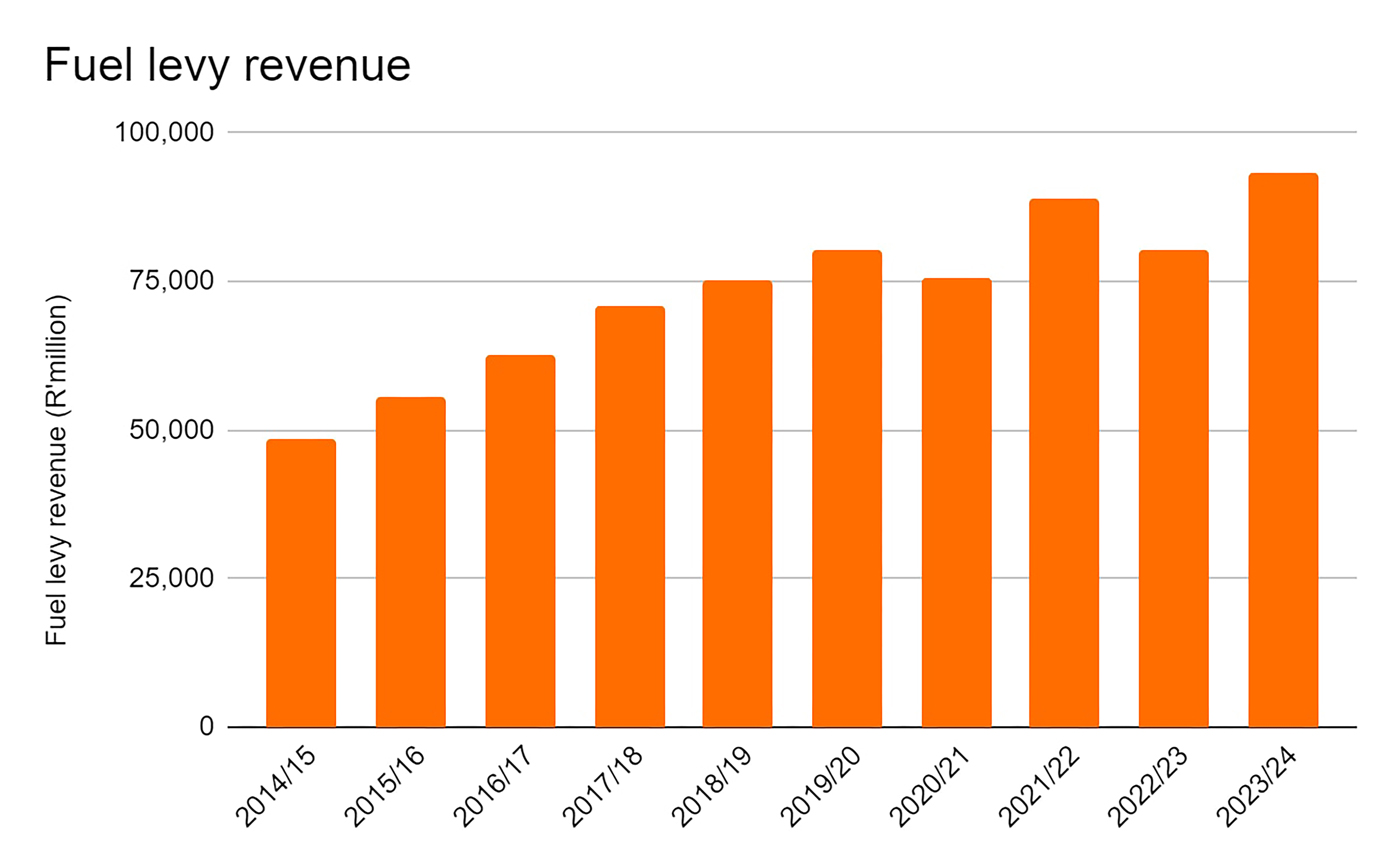

With a growing number of vehicles on the road, more available public transport, increasing road freight, and escalations in the fuel levy, this has brought in a tidy sum of money to the fiscus over the years, with very little finding its way into the roads.

Ironically, at the time of consultations over the Gauteng Freeway Improvement Project (e-toll), which has now been scrapped, the transport industry was told that – due to the buoyancy of the fuel levy – it could not be utilised to pay for the e-tolls and required a user-pay approach. Years later, however, it is now a stable enough mechanism to fill the state’s coffers (or is this perhaps an act of desperation?).

Godongwana also announced that the 2026 Budget would propose tax measures to raise an additional R20 billion in revenue. He did not provide any indication as to where this will originate from, so we will have to brace ourselves for more shock announcements in the coming months.