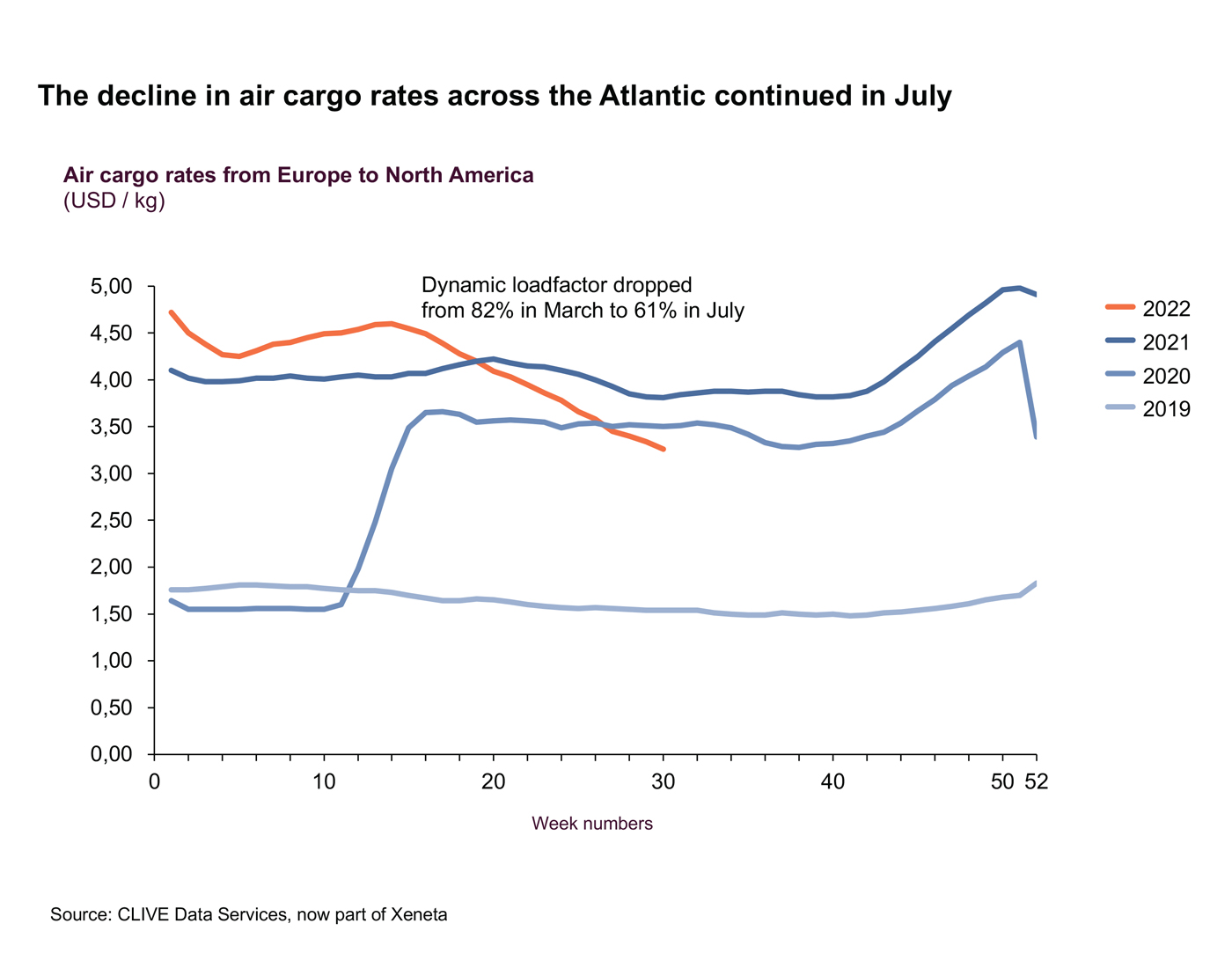

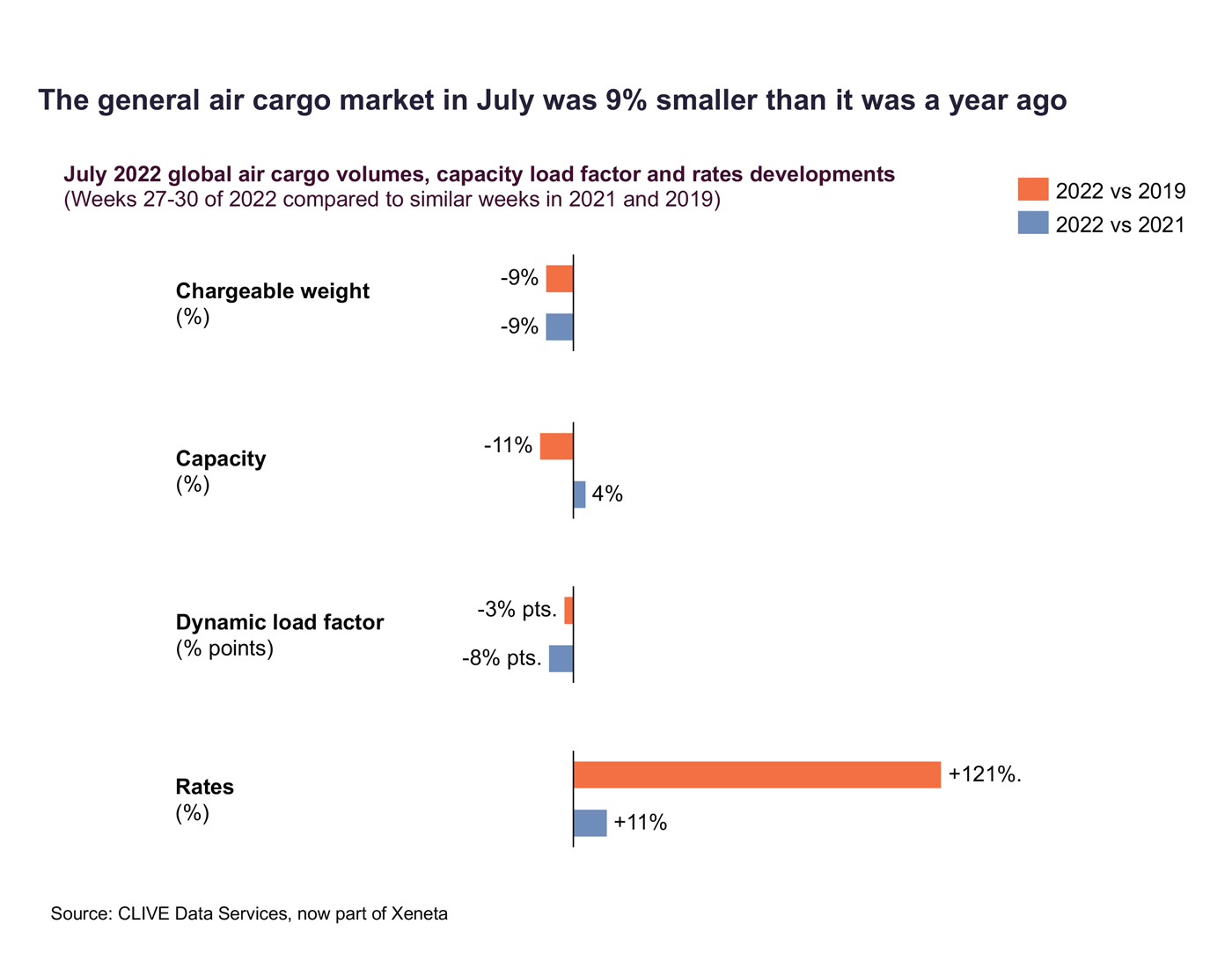

Seasonally adjusted general air cargo market performance data shows a continued slowing down of volume, load factor, capacity, and airfreight rates as the impact of economic and political uncertainties on world trade continue to hang over the industry.

Weekly market intelligence from industry analysts CLIVE Data Services, now part of Xeneta, shows volumes dropped by 9% in the first month of the third quarter compared to July 2021. Demand was also down by 9% versus the same month of 2019. Capacity growth slowed to just 4% over the July 2021 level and was 11% down compared to July 2019. This caused CLIVE’S dynamic load factor measure to drop eight percentage points year-over-year to 58%, taking into consideration both the weight and volume of cargo flown, and the capacity available, to produce the most accurate indicator of airline performance.

Airfreight rates also continued to fall in July, relative to the June 2022 year-over-year analyses, CLIVE reports, although they remain at +121% versus July 2019 and +11% compared to the same month a year ago.

The slowdown in the global air cargo market since March 2022 is ongoing, says Niall van de Wouw, founder of CLIVE and chief airfreight officer at Xeneta. There has been no let-up in the multitude of disruptions outside of the industry’s control, from uncertainties caused by the continuing war in Ukraine to the escalating cost of living crisis and its impact on household budgets and business performance. Latest reports in the Netherlands, for example, show supermarket rates for groceries 20% higher on average compared to 11 months ago. This is further impacting the discretionary spending of consumers. Closer to home, airlines and airports continue to suffer severe operational challenges due to significant shortages of ground staff.

{kind=link}

{kind=link}