Conflict in the red sea disrupting ocean freight services has been an immensely impactful “black swan” event for air cargo. Charleen Clarke reports that there have been +11% increases in global air freight demand for the fourth straight month, partially as a result of the unrest.

The global air cargo market is on the boil! According to Global Market Insights, the global air cargo market was estimated at US$200 billion in 2022 and is anticipated to hit US$300 billion by 2032, thanks to the rising need to transport high-value and time-sensitive products such as electronics, perishable goods, auto parts, and pharmaceuticals.

Growth is already being seen, and the International Air Transport Association (IATA) has just released data for March 2024 global air cargo markets that show continuing strong annual growth in demand. Total demand, measured in cargo tonne-kilometres (CTKs), rose by 10.3% compared to March 2023 levels. This is the fourth consecutive month of double-digit year-on-year (YoY) growth. The 10.3% YoY growth in industry CTKs was driven by traffic on international routes, which expanded by 11.4% YoY in March, helped by the rapidly increasing demand for e-commerce services. Importantly, all regions experienced both month-on-month (MoM) and YoY expansions, the former in double digits and the latter in excess of 3%.

International CTKs of airlines registered in the Middle East and Africa posted the highest annual growth rates, with 19.9% and 14.1% respectively. These airlines were closely followed by those registered in Asia Pacific (13.8%), Europe (10.0%), and Latin America (7.8%). North American carriers experienced the lowest YoY growth with 3.1%. IATA maintains that carriers are likely benefiting from continued conflict and drought-induced disruptions in the Suez and Panama Canals, which have been affecting global maritime shipping capacity.

Capacity, measured in available cargo tonne-kilometres (ACTKs), increased by 7.3% compared to March 2023 (10.5% for international operations).

“Air cargo demand grew by 10.3% over the previous March. This contributed to a strong first quarter performance which slightly exceeded even the exceptionally strong 2021 first quarter performance during the Covid crisis. With global cross-border trade and industrial production continuing to show a moderate upward trend, 2024 is shaping up to be a solid year for air cargo,” says Willie Walsh, IATA director general.

April sees growth

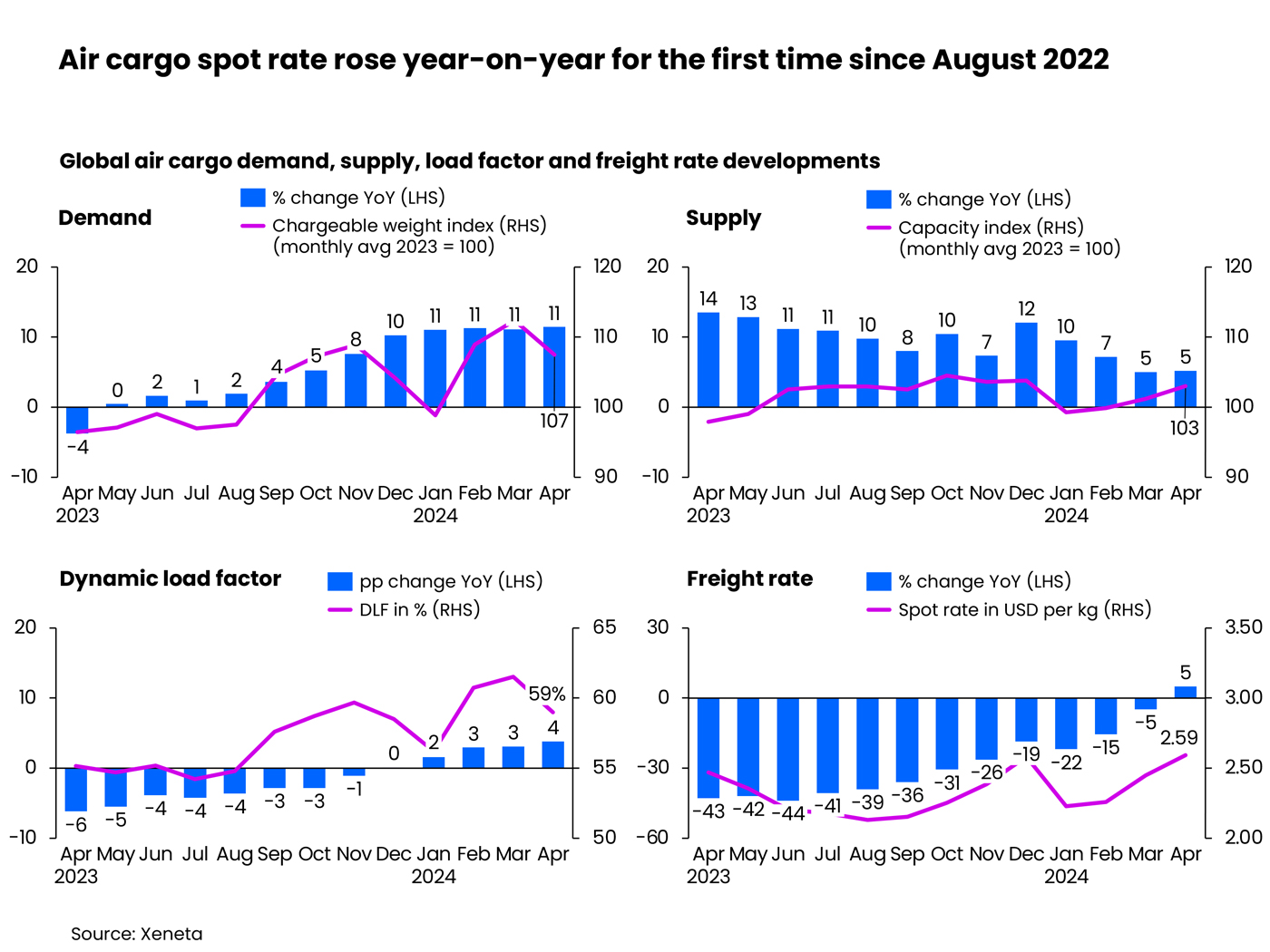

Meanwhile, Xeneta has just released its latest data analysis, which reveals that April registered the fourth straight month of +11% increases in global air freight demand. The injection of extra cargo capacity as airlines launched their (European) summer schedules boosted supply growth by +5% YoY in April. This placed expected downward pressure on the so-called “dynamic load factor”, dropping from 62% in March to 59% in April. The dynamic load factor is Xeneta’s measurement of cargo capacity utilisation based on the volume and weight of cargo flown alongside the available capacity.

In April, YoY growth of the global air cargo spot rate turned positive for the first time since August 2022, increasing by 5% due to a combination of Middle East conflicts and strong e-commerce demand. As a result, the average global spot rate rose to US$2.59/kg, its highest level this year.